The latest DFC Intelligence report shows the number of global video game consumers has soared to 3.7 billion. This is closing in on nearly half of the global population as video games become ubiquitous. The new numbers were reported as part of the latest release in the DFC Video Game Consumer Segmentation service.

The reality is the overall number of video game consumers is fairly meaningless and mainly used for grabbing headlines. The actual core consumer base is only about 10% of the 3.7 billion. Furthermore, that 10% needs to be further sub-segmented to obtain the true addressable market for a specific product.

Currently, the biggest focus for the core game industry is naturally on targeting the 300 million hardware-driven consumers. These are the consumers that buy dedicated systems to play games, whether it be a console system or a gaming PC. This audience is growing, but not nearly as fast as the global audience which is driven by being able to play games on mobile phones.

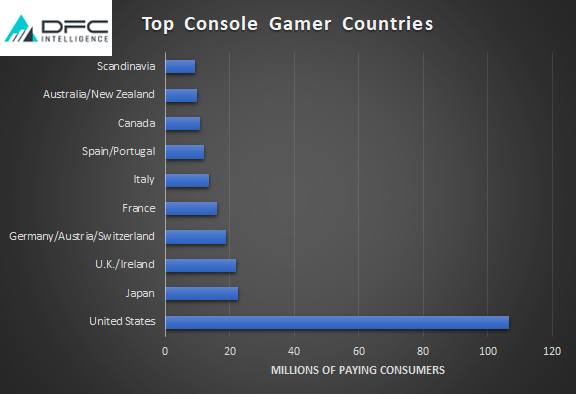

There is a large disparity between where the core audience is located. Console video game consumers are heavily weighted towards North America and Europe. Mobile game consumers, by far the largest segment, are more representative of the global population.

Getting mobile-only consumers to upgrade to a larger screen is a major opportunity. However, it will not be easy and most companies in the game space are smart to narrow their focus to core consumers. Nevertheless, there is definitely an opportunity to expand the video game hardware business.

Over the next decade, there is likely to be a significant change in the hardware used to play games as more devices look to reach a broader audience. This could be through the growth of cloud game handheld platforms that are starting to flood the market. However, it is more likely to be through a hybrid ecosystem that allows for multiple styles of gameplay.

In the console market, Nintendo is the only company that has significantly grown its audience in recent years with the hybrid console/portable Nintendo Switch. The Switch works as both a handheld, as well as docked to a larger monitor. Nevertheless, the Nintendo audience remains relatively limited and Nintendo as a company has a narrow focus.

In other words, the next decade is wide open for potential innovation in the video game industry hardware market. Cloud delivery can expand distribution, but end users will always need hardware to play games. At the very least, a monitor and control system.

Smartphones with touch screens are serving as an entry point for billions of global consumers. The next challenge for the video game industry is figuring out how to upgrade those consumers to the next level.

In addition to the new video game consumer report. The new DFC console forecasts have just been released. For a full discussion of these issues and recent company performance, see the latest DFC Intelligence quarterly video game market overview.