Video Game Industry Segments: Games as a Service versus Traditional Games

The recent DFC report The Business of Video Games breaks the game industry into multiple segments. At a high level the biggest distinction is between traditional pay-to-play games and games as a service. These are almost two entirely separate businesses and it will be interesting to see how many companies can play in both segments.

Overview

Pay-to-play is what most people think of as the traditional console video game industry. A developer creates a game, a publisher puts it in a box and ships it to retailers where consumers go in and buy it for a set price. Of course, as games go digital, publishers don’t necessarily need to package the game in a box.

The concept of games as a service has evolved from persistent online games. These are games consistently changing as both users and developers add to the product. In many cases these are entirely free games that are monetized via virtual currency that is used to buy in-game content.

Games can be further divided by platform and whether they are a premium game with big budget development costs or a low-end game with more modest development costs.

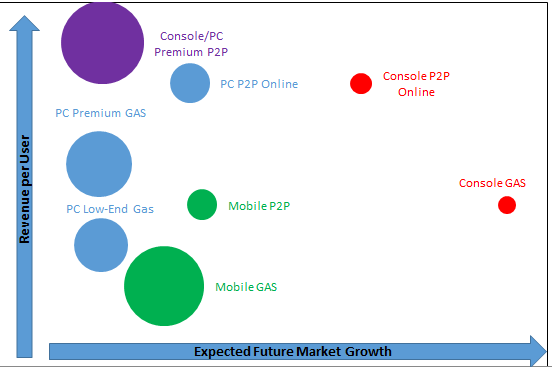

The bubble chart divides games into 8 segments and analyzes how direct consumer spending breaks down now and is expected to grow in the future (in this analysis, advertising spending is not included but is a growing source, especially for mobile).

The size of the bubble indicates the current market size based on direct consumer spending. The vertical axis represents how much revenue per user the segment generates. The horizontal axis measures expected growth over the next five years.

Market Segments

1. Console/PC Premium Pay-to-Play: These are the big games that will make noise this fall like the latest Call of Duty, Battlefield, Super Smash Bros. etc.

2. PC Pay-to-Play Online: These are many of the games you find on Steam. In many cases they come from indie developers.

3. Console Pay-to-Play Online: Sony, Microsoft and Nintendo all have a growing business of publishing digital only games from smaller developers on their console platforms.

4. Mobile Pay-to-Play: These are mobile games that attempt to charge users a set fee to play, such as Nintendo’s Super Mario Run.

5. Mobile Games as a Service: This is the business model for most of the major mobile games.

6. PC Low-End Games as a Service: There is growing crossover between Low-End PC games as a service and mobile games. As we discussed in the Business of Video Game report and a recent article, many PC companies in this segment, such as Zynga, are moving more towards mobile.

7. PC Premium Games as a Service: With games like World of Warcraft, the Blizzard portion of Activision Blizzard has been a leader in this category. In this case there has also been some success in also getting consumers to pay upfront. As we discussed last week, NCSoft enjoyed some great recent success bringing their Lineage game to mobile platforms.

8. Console Games as a Service: The best example of this category is the recent success of Fortnite for the console platforms. Overall, this is the smallest segment but it has the greatest growth potential.

Conclusion

A big question we are examining is how well the large publishers are moving from premium P2P games to GAS. This is a critical issue for the industry. Pay-to-play games generate high revenue per user but the games as a service model is proving very popular. The question many investors are asking is can game companies have their cake and eat it too?

We encourage you to check out the new video game industry segmentation that DFC Intelligence did in conjunction with Venture Beat and Atlas Technology Group. It is available on the Venture Beat website.